U.S. Biofuels Market and Used Cooking Oil (UCO) – A Comprehensive Data Review

- Becks Sanitation

- Jul 8, 2025

- 15 min read

Updated: Jul 9, 2025

Introduction: UCO as a Key Biofuel Feedstock

Used cooking oil (UCO) has emerged as a critical low-carbon feedstock for biofuels like biodiesel, renewable diesel, and sustainable aviation fuel (SAF). Converting waste oils into fuel not only diverts waste from landfills but also provides “better, cleaner fuels” that help decarbonize transport . UCO is prized for its low carbon intensity (CI) under clean fuel standards, but its supply is inherently limited as a waste byproduct. This review compiles data from recent reports and news to analyze UCO supply, demand, trade flows, and how policies are shaping the U.S. market. We focus on the U.S. context, with relevant global insights, to provide an in-depth, data-driven overview of the UCO and biofuels landscape.

UCO Supply and Demand: Global and U.S. Overview

Global UCO Supply: In 2022, global available UCO supply was estimated around 3.7 billion gallons (≈14 billion liters). This supply comes predominantly from restaurant and food-industry waste oils collected worldwide. UCO collection has historically been driven by waste disposal regulations, but in the last decade biofuel policies (especially in the EU and California) have become the key demand driver. Approximately 80% of UCO collected globally is now used for biofuel production (only ~20% goes to lower-value uses like animal feed), as shown in the pie chart below. Stricter rules (e.g. banning waste oil in livestock feed) have further shifted UCO away from those traditional uses and into fuel markets.

Global consumption of UCO by sector in 2022 (biofuels vs other uses). Roughly 80% is utilized in biofuel production, reflecting policy-driven demand for low-carbon feedstocks.

U.S. UCO Supply: The United States has one of the most developed UCO collection networks in the world. In 2022, U.S. UCO collection (including “yellow grease,” i.e. used fryer oil) reached about 0.85 billion gallons. This robust collection is aided by America’s high per-capita consumption of vegetable oil and wellestablished recycling practices. In fact, roughly one-quarter of the cooking oil used in U.S. food service is recovered as UCO. By comparison, China only recovers ~15% of its used cooking oil, indicating room for expansion there. Because the U.S. already captures a large share of its waste oil, growth in U.S. UCO supply is expected to be modest – per-capita collection was ~2.5 gallons/person in 2022 and could reach ~3.2 by 2030 (yielding about 1.1 billion gallons supply in 2030). This means domestic UCO alone cannot fuel the nation’s entire clean-fuel ambitions, and other feedstocks must fill the gap.

Booming Biofuel Demand: Demand for UCO is rising in tandem with the rapid growth of bio-based diesel fuels. U.S. consumption of biodiesel and renewable diesel has been climbing, with 2024 on pace to exceed 5 billion gallons for the first time (up from ~3 billion in 2016). Renewable diesel capacity in particular has surged, creating strain in feedstock markets. UCO is an attractive feedstock because it yields fuels with very low lifecycle carbon emissions, qualifying for premium credits under programs like California’s Low Carbon Fuel Standard (LCFS) and the Renewable Fuel Standard (RFS). However, UCO supply is finite – it is “one of the most readily available waste greases globally,” but inherently limited by the amount of cooking oil consumed and collected. This has led to pressing questions about whether UCO supply can scale up enough to meet aggressive clean fuel targets.

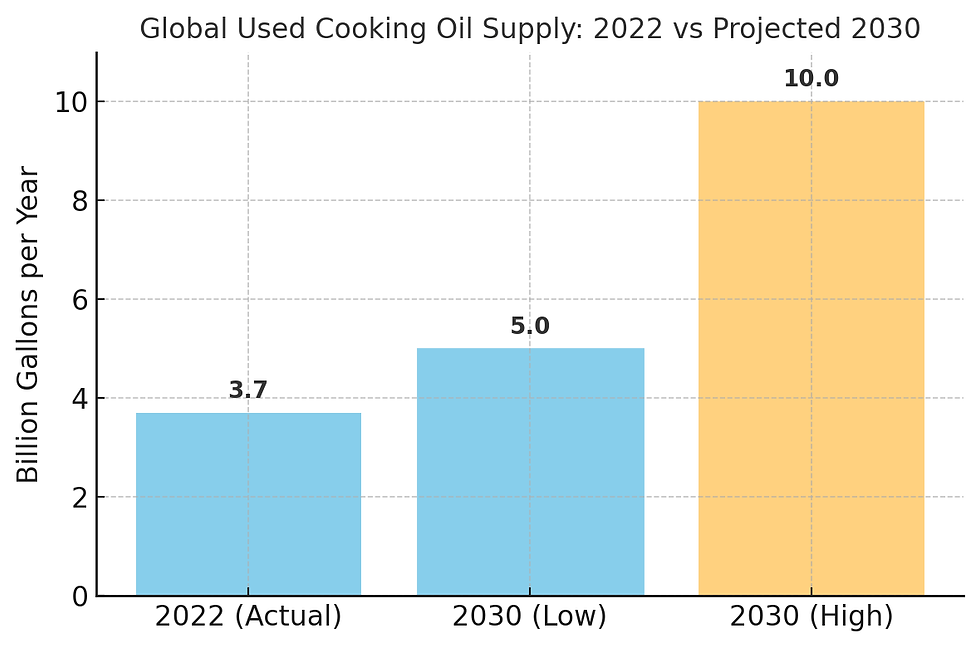

To illustrate future projections, the chart below shows global UCO supply in 2022 vs. 2030. Analysts project a significant increase by 2030, driven by expanded collection and rising biofuel demand:

Global used cooking oil supply in 2022 (actual) compared to projected 2030 scenarios. By 2030, global UCO availability is forecast to reach 5–10 billion gallons per year.

As shown, global UCO output could roughly double from 3.7 billion gallons in 2022 to 5–10 billion gallons by 2030. The wide range reflects different scenarios – the lower end assumes current collection trends, while the upper end assumes maximal expansion of collection networks worldwide. Industry experts note there is “further upside potential” beyond 10 billion if more countries implement UCO recycling, but overcoming logistical barriers (infrastructure, public participation, etc.) will require continued incentives. In a full best-case, total global UCO supply by 2030 could approach ~17 billion gallons with concerted effort. However, reaching that level would likely extend beyond 2030 and need supportive policies and investments to “overcome barriers” in countries that currently collect little to no UCO.

Summary of Key UCO Metrics: The table below highlights some key data points about UCO supply, trade, and projections, based on the latest available sources:

Metric | Value / Trend |

2022 Global UCO Supply | ~3.7 billion gallons |

2022 U.S. UCO Collection | ~0.85 billion gallons (≈23% of global) |

2022 Global UCO Exports (Trade) | ~1.3 billion gallons (about one-third of supply) |

China’s UCO Exports (2024) | ~3 million metric tons (≈0.9 billion gal) (record high) |

UCO Imports to U.S. (2023) | ~3× increase vs 2022 (50% came from China) |

Tariff on Chinese UCO (Apr 2025) | 125% import duty (effectively halting imports) |

2030 Projected Global UCO Supply | 5–10 billion gallons (additional potential to 17B) |

2030 Projected U.S. UCO Supply | ~1.1 billion gallons (limited growth due to high current collection) |

Table: Key data on UCO supply, trade, and projections.

The Impact of Chinese UCO on U.S. Biofuel Markets

In recent years, China has become the world’s largest exporter of UCO, and this has significantly affected the U.S. biodiesel/renewable diesel market. In 2022–2023, U.S. imports of UCO surged, largely due to cheap supply from China. Imports of used cooking oil into the U.S. tripled from 2022 to 2023, with 50% of those imports coming from China. Chinese UCO was cheaper than domestic feedstock (like U.S. soybean oil), so fuel producers eagerly bought it to reduce costs . This helped U.S. biofuel producers meet growing demand for low-CI feedstock, but it also undercut U.S. agriculture – reducing demand (and prices) for domestic soy oil and other vegetable oils . In short, Chinese waste oil was eroding U.S. farmers’ market share in the burgeoning renewable fuel industry.

Tensions came to a head in late 2024. U.S. farmer groups protested what they called a “climate law loophole” – essentially, they argued that policy incentives for low-carbon fuels were unintentionally favoring imported Chinese UCO over American-grown crops. They urged the White House to act, fearing that cheap UCO imports were displacing demand for soybeans and other “green fuel” crops. Biofuel 2 3 3 trade organizations for soy farmers and oilseed processors lobbied for intervention, claiming some Chinese UCO might not even be genuine (more on that below), and that allowing it free entry “subverted” the intent to support domestic feedstocks.

Policy Response – Tariffs: The calls for action were heard. Beginning in April 2025, the U.S. government imposed a steep 125% import tariff on UCO from China. This effectively shut off Chinese UCO flows to the U.S. – a dramatic market shift. Prior to the tariff, the U.S. had been China’s largest UCO customer, with shipments worth $1.1 billion in 2024. China’s total UCO exports hit an all-time high in 2024 of nearly 3 million metric tons (worth $2.64 billion), so the U.S. accounted for roughly 40% of China’s export value. The new 125% duty closed that arbitrage. By April 2025, the last few UCO cargoes from China were arriving in U.S. ports; thereafter trade ground to a halt. “For the time being, arbitrage to the U.S. is closed and we think it will remain so in the medium term,” said one major Chinese UCO trader.

U.S. biofuel producers have had to adapt quickly. Some warned of negative impacts from cutting off imports – noting that domestic low-CI feedstocks were already in short supply and expensive . The Advanced Biofuels Association cautioned that tariffs could be a “governmental overreach” that might inadvertently hurt the fuel industry by straining feedstock supply . On the other hand, U.S. farmers welcomed the protection; soy oil prices and demand were expected to firm up as domestic feedstocks replace the lost Chinese UCO. Indeed, U.S. renewable diesel plants may need to pivot to relying more on homegrown oils and other waste fats (like used animal tallow or distillers corn oil) in the absence of Chinese imports.

China Pivots to Europe and Asia: From China’s perspective, the loss of the U.S. market forced a redirection of exports. Chinese suppliers are now pivoting to Europe and other Asian countries. “Some of the exports will be diverted to Europe and new markets in Asia such as Korea, Thailand, Malaysia and India,” according to trading executives in Shanghai. Europe is a natural destination because the EU strongly incentivizes waste oils for biodiesel (through its Renewable Energy Directive’s double-counting mechanism) and has new SAF blending mandates kicking in. In fact, the EU began requiring at least 2% SAF in jet fuel in 2025, and traders predict Europe will become the top buyer for at least half of China’s UCO exports in coming months .

Other Asian countries are also increasing imports – notably Singapore, South Korea, and Malaysia, which have biodiesel/renewable diesel refining hubs. Some Southeast Asian nations act as consolidators: smaller UCO shipments from across Asia (including China) are aggregated, then re-exported in bulk. Malaysia, for example, has become a key hub for regional UCO trade. This intra-Asia trade is significant; even when China was sending UCO to the U.S., it also imported some UCO from neighboring countries to blend and export. Now, with the U.S. market largely closed, China’s UCO exports to EU and regional biofuel plants are set to increase, though total Chinese export volume will likely drop (since the U.S. was its biggest buyer).

Declining Chinese Exports & Rising Domestic Use: It’s important to note that China’s overall UCO exports were expected to fall in 2025 regardless of tariffs, due to internal changes. As of January 2025, Beijing removed a tax rebate that had previously incentivized UCO exports. Moreover, the U.S. Inflation Reduction Act introduced a new “clean fuel” tax credit policy that discourages use of imported UCO in U.S. biofuels. These policy shifts had already slowed shipments in late 2024. With the tariff on top, Chinese UCO exports are now projected to plunge by 20–40% in volume. Traders estimate China’s export volume will 4 5 6 4 settle at ~150,000–200,000 tons per month from Q2 2025 onward – down from ~250–300k tons/month last year.

At the same time, China’s domestic demand for UCO is rising. The country has launched its own sustainable aviation fuel (SAF) industry, which uses UCO as a major feedstock. At least four new SAF facilities in Asia (including Thailand, Malaysia, Japan) came online by 2025 with ~700,000 tons per year capacity combined, and several are in China. For example, China’s Zhejiang Jiaao and Blue Whale Bioenergy started SAF production in late 2024/early 2025, and other plants (Haixin Energy, Haike Chemical) are slated to begin soon . Chinese SAF producers were already consuming 100,000–120,000 tons of UCO each month in early 2025, a figure expected to climb as new plants ramp up. In short, China is using more of its UCO at home to produce SAF and renewable fuels for its nascent clean energy goals. (China even launched a pilot program in Sept 2024 to use SAF on domestic flights at several airports.)

The combined effect of all this: Chinese UCO that once flooded into the U.S. is now largely staying in Asia or heading to Europe. The U.S. biofuel market has lost a major source of low-cost feedstock virtually overnight, which will test how robust the domestic supply system is – and whether other import sources (e.g. used oil from Latin America or Canada) can fill the gap.

Quality and Sustainability Concerns: “Tainted” UCO and Market Integrity

Beyond economics, questions about the quality and authenticity of some imported UCO have troubled regulators and industry leaders. There have been allegations that some of China’s exported UCO was “tainted” by mixing with cheaper oils like palm oil. In other words, unscrupulous actors could dilute genuine used cooking oil with virgin palm oil (from Southeast Asian plantations), yet still sell it as “wastederived” fuel feedstock – reaping financial rewards from the higher credit value of UCO. Palm oil masquerading as UCO undermines the climate benefits (palm cultivation can drive deforestation) and violates the spirit of clean fuels programs.

Such fraud accusations are not new. Europe previously raised concerns that Chinese exporters were blending palm oil into UCO shipments to take advantage of EU incentives for waste oils. These claims put Chinese UCO under scrutiny on both sides of the Atlantic. The Renewable Fuel Standard in the U.S. requires that biofuel feedstocks meet the definition of renewable waste biomass and that detailed records trace the supply chain. If palm oil or other non-qualifying oils are mixed in and not reported, that would be illegal under the RFS.

U.S. regulators have taken notice. EPA officials confirmed in 2024 that they were monitoring the spike in imported UCO closely. RFS rules mandate that producers using waste oils maintain documentation from collection to fuel production, to prove the feedstock’s authenticity and eligibility. The EPA and industry groups like the National Oilseed Processors Association grew increasingly vocal about ensuring waste oil feedstocks are legitimate. Geoff Cooper, CEO of the Renewable Fuels Association, warned that if fraudulent UCO is not checked, “it could potentially undermine the integrity of the Renewable Fuel Standard.” In other words, widespread fake “renewable” feedstock could erode confidence in the whole system.

These quality concerns added another rationale for limiting Chinese UCO imports. Even before the tariff, some in the U.S. biofuels industry were uneasy about heavy reliance on a feedstock half a world away with 7 5 murky supply chains. The possibility (even just the perception) of tainted UCO from abroad could tarnish the environmental reputation of biodiesel/renewable diesel – at a time when these fuels are competing with electrification and other strategies for support. Thus, the crackdown on Chinese UCO can be seen as motivated by both economic protectionism and environmental fraud prevention. Moving forward, any imported UCO that does enter the U.S. from other countries will likely face similar scrutiny to ensure it’s truly waste oil.

Policies and Market Adjustments in the U.S.

The U.S. clean fuels landscape is shaped by a mix of federal and state policies, which together drive demand for feedstocks like UCO while also setting guidelines on their use:

Renewable Fuel Standard (RFS): At the federal level, the RFS mandates annual volumes of biofuel blending. UCO-based biodiesel qualifies as an advanced biofuel (D4 Renewable Identification Numbers) under RFS due to its high greenhouse gas reduction. The EPA’s oversight (as noted) is crucial to ensure RFS credits aren’t generated fraudulently. The influx of UCO raised RFS compliance questions – but with imports now curtailed, RFS will lean more on domestic feedstocks and other advanced fuels (like renewable natural gas, etc.) to meet targets.

Blender’s Tax Credit and New Production Tax Credit: A long-standing $1/gal biodiesel blender’s tax credit (BTC) helped make UCO-based biodiesel competitive. That credit is now phasing into a new Clean Fuel Production Credit (CFPC) under the Inflation Reduction Act. Starting in 2025, the CFPC (Section 45Z) will reward producers of fuels based on carbon-intensity: the lower the CI, the higher the credit. This may indirectly discourage imported UCO, because any added emissions from transporting feedstock thousands of miles will count toward CI. Moreover, the IRA’s SAF-specific credit (up to $1.75/gal) has strict lifecycle and feedstock sustainability requirements. Reuters reported that the “new U.S. clean fuel tax policy…discourages the use of imported UCO” – likely referencing these IRA provisions that favor local sourcing or at least penalize carbon-intensive supply chains. In effect, federal tax incentives are aligning with the goal of promoting domestic waste resources and truly low-carbon inputs.

State Low-Carbon Fuel Standards: California’s LCFS and similar programs (e.g. Oregon’s Clean Fuels Program, Washington’s new Clean Fuel Standard) create a credit market for low-CI fuels. These programs have strongly driven UCO demand because fuels made from UCO generate far more credits (due to ~80–90% GHG reduction vs petroleum) than fuels from crop-based oils. Credit prices can be volatile, however, if supply lags demand. For instance, Oregon’s Clean Fuels Program saw credit prices spike, prompting the implementation of a Credit Clearance Market mechanism to cap prices around $200+/tonne and ensure compliance flexibility. Such measures indicate how tight the market for waste-based fuel is – there is only so much UCO and similar feedstock to go around, and when multiple states compete for them, credit prices (the incentive) rise until either more supply comes or a safety valve is hit. With Chinese UCO off the table, West Coast programs may face higher credit prices or will need to source more alternative feedstocks (e.g. used fats from Latin America, or ramp up local collection of greases).

Trade Policy and Import Diversification: The 125% tariff on Chinese UCO is the most dramatic trade measure, but there’s also an eye on other import sources. The U.S. brings in some used cooking oil from Canada and parts of Latin America. These sources might increase in the short • • • • 6 term to partially offset the loss of Chinese volumes. However, none have the scale China did. Policymakers will have to balance feedstock supply needs vs. sustainability. If, say, Southeast Asian UCO (from Indonesia, Malaysia) is available, should it be encouraged to supply U.S. refineries? Or would that carry similar fraud/deforestation concerns as the Chinese supply? These are ongoing policy considerations as the U.S. aims to both grow its biofuels output and ensure it is “clean” in truth, not just on paper.

In summary, U.S. policy is increasingly favoring local, sustainable feedstocks and putting guardrails to prevent market distortions. The combined federal and state actions are pushing the industry toward developing new feedstock sources (from cover crops like camelina, to algal oils, to expanded waste collection from municipalities) so that the clean fuels growth can continue without hitting a hard wall on feedstock limits.

Broader U.S. Bioeconomy Efforts and Future Outlook

The focus on used cooking oil is part of a larger push to build a low-carbon bioeconomy in the United States. The U.S. Department of Energy’s Bioenergy Technologies Office (BETO) projects that domestic biomass and waste resources could sustainably produce up to 50 billion gallons of biofuels per year for aviation, marine, and heavy transport, along with biopower and renewable chemicals – contributing to a 450 million metric ton annual CO₂ reduction if fully realized. These figures illustrate the enormous scale of the opportunity: biofuels and bioproducts can play a major role in decarbonizing sectors that are hard to electrify (like long-haul trucking, aviation, and industrial processes).

Investment and Innovation: To tap this potential, government and industry are investing in research, development, and deployment of new technologies. BETO’s strategy is to “de-risk” bioenergy tech through R&D across the value chain – from feedstock production (e.g. energy crops, waste collection logistics) to conversion (more efficient bio-refineries). Recent initiatives include funding for community-scale waste-toenergy projects that help cities turn organic waste (food scraps, municipal sludge, landfill gases) into fuels and power. Such projects not only reduce landfill methane but also create local feedstock sources for energy, complementing feedstocks like UCO. The DOE announced in late 2024 a planned $23 million funding opportunity to assist communities in developing strategies to convert their organic waste streams into bioenergy feedstocks. This kind of support will help broaden the pool of “waste” feedstocks beyond just used cooking oil – sewer grease, agricultural residues, yard waste, etc. can all contribute to the clean fuel supply.

Expanding Feedstock Supply: The Clean Fuels Alliance America (formerly National Biodiesel Board) recognizes the need for more feedstock. “Growing demand for better, cleaner fuels like biodiesel, renewable diesel and SAF is creating a tremendous opportunity to develop additional supplies of low-carbon fats and oils, including used cooking oil and surplus crop oils,” said Clean Fuels CEO Donnell Rehagen . The industry’s vision is to sustainably produce 6 billion gallons of biodiesel/renewable diesel/SAF by 2030. Meeting this goal will require “crucial additional feedstocks” – from increasing UCO collection globally to tapping non-food oils (e.g. pennycress, carinata, algae) and improving yields of byproduct oils (like distillers corn oil from ethanol plants). The global UCO outlook report identified that with improved collection, an extra 4–7 billion gallons of UCO could potentially be realized worldwide on top of baseline growth. Capturing this potential will involve everything from public awareness (encouraging restaurants in all countries to recycle their fryer oil) to infrastructure (more collection trucks and processing centers in developing regions).

Recognition and Collaboration: Progress is being made on multiple fronts. In 2023, industry and policymakers celebrated “Globally Recognized Trailblazers” in advancing clean fuels (for example, innovators who set up large-scale UCO recycling programs or produced breakthrough SAF from waste). The Environmental and Energy Study Institute (EESI) and other nonprofits regularly highlight solutions – such as indigenous agricultural practices and circular economies – that tie into the bioeconomy’s growth. There is also an Interagency Bioeconomy Initiative working to improve data and coordination across USDA, DOE, EPA, etc., to support a data-driven expansion of the U.S. bioeconomy. This group released a report in mid-2023 outlining needs for better data collection on biomass resources and supply chain logistics, which will help identify where feedstock supplies can be expanded or where policy tweaks are needed.

Sustainable Scale-Up: While the near-term UCO market is tight, the bigger picture for the biofuels/ bioenergy sector remains one of growth and innovation. The U.S. aims to scale up without sparking sustainability issues (like food-vs-fuel conflicts or habitat loss). That means waste and residue feedstocks will be the priority wherever possible. Used cooking oil is a great example of a true waste feedstock that adds value and cuts emissions – but it’s just one piece of the puzzle. Other waste streams (e.g. animal fats, forest residues, municipal solid waste, even captured CO₂ combined with green hydrogen to make fuels) are being explored and deployed.

In conclusion, the data tells a story of both opportunity and limits. UCO has become a prized commodity in the clean fuels industry, and demand for it has skyrocketed in the U.S. and globally due to policy incentives. However, its finite supply and the recent disruption of Chinese imports reveal the fragility in relying too much on any single feedstock. Moving forward, the U.S. industry will need to diversify feedstocks and strengthen domestic supply chains, while global cooperation can help raise collection rates abroad. With supportive policies and innovation, the biofuels sector is poised to grow – but it must do so by sustainably scaling the entire bioeconomy, turning more waste into fuel and ensuring robust verification to maintain credibility. As the DOE notes, the U.S. has a “wealth of sustainable biomass and waste resources” that can be mobilized for a thriving bioeconomy. The UCO experience of the past two years underscores both the importance of those resources and the need for smart strategies to manage them for the climate benefit of all.

Sources

Reuters – “China pivots to Europe for used cooking oil exports as tariffs hit shipments to US”, Apr. 30, 2025 .

ResourceWise – “Chinese Used Cooking Oil Disrupts US Biodiesel Market”, May 23, 2024 .

Clean Fuels Alliance (via Biofuels Int’l) – “Clean Fuels releases outlook for global supplies of UCO”, Sep. 14, 2023 .

Clean Fuels Alliance – Global UCO Supply Report (LMC/GlobalData), Sep. 2023 .

EIA / Biodiesel Magazine – U.S. biodiesel & renewable diesel market stats 2024 .

Energy.gov – “Building a Low-Carbon U.S. Bioeconomy” (BETO fact sheet), 2023 .

Oregon DEQ – Clean Fuels Program Credit Clearance Market (website) .

EESI – Climate Change Solutions Newsletter, Sep. 19, 2023 .

Clean Fuels Alliance – Press release quotes (Donnell Rehagen) .

Great article. At Biocoils (Chile)♻️🇨🇱, we specialize in the collection and preparation of used cooking oil (UCO) for biodiesel production.

We have the capacity to export large volumes and are looking for partnerships with buyers committed to sustainability.

More information at 🌐 www.biocoils.cl 🔹 Instagram 🔹 Facebook 🔹 LinkedIn